31 Oct 2025

Who we can help: Are you making the most of your retirement investments?

A good retirement plan is as much about your withdrawal choices in retirement, as it is about the capital you accumulate on the way. It can make a significant difference to your overall retirement outcomes, in what order you utilise your different investments and how these withdrawals are impacted by tax.

Until recently, many people looked to first utilise tax-free accounts – for example taking a tax-free lump sum from their pension, then ISA withdrawals, then accounts that were subject to on-going taxes such as a general investment account, and only later in retirement did they consider withdrawals from their remaining pension pot, because this income is typically withdrawn at your marginal tax rate.

This order of use can still be appropriate for those whose total estate, including property and other possessions, is less than £500k for a single person or £1m for a couple.

Here’s an example of the difference that the order of use of accounts might make over the course of a retirement.

Mr Scramble is 67 years old and has just retired. He is entitled to the full state pension, which supports part of his total expenditure requirement of £35,000 per year. He has the following accounts:

- A general investment account £50,000

- An ISA account with £125,000

- A personal pension that has not yet been accessed with £250,000

The total value of his liquid investments is £425,000 and all of these accounts are invested in a Moderate portfolio (also known as a Balanced portfolio of circa 60% Equities, 40% Fixed Income).

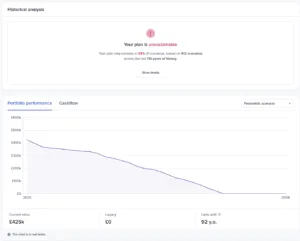

Based on a strategy of withdrawing income proportionately from each account (meaning that income is taken in proportionate amounts to the relative size of the General Account, ISA and personal pension), the cashflow forecast shows that in a pessimistic scenario, the plan will survive approximately 43% of the time. This means that up to 57% of the time, if market conditions are not good (as per pessimistic scenario planning) he will run out of money before he dies, with a projection that his funds will typically last until he is 92 years old..

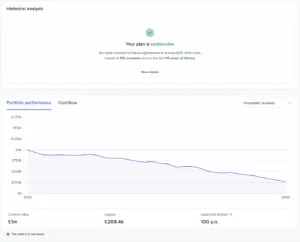

However, if a few tweaks are made the sustainability of the plan can be substantially increased. For example, if the use order is amended so that the pension is only used to provide income later in retirement, and if within the pension, the portion which will only be used later is invested more aggressively, then this allows the overall projected success of the plan to increase significantly. This does not have to mean an increase in overall risk exposure, as those funds which will be spent in the earlier years (e.g. from the general account) can be invested in a less risky way to balance out the overall risk exposure of the total portfolio. With the same starting assets on retirement but a different withdrawal and investment strategy, the model now shows a successful plan 72% of the time even in a pessimistic scenario, and a projected legacy of £108k remaining at age 100.

So we can see that for Mr Scramble, as for many others obtaining retirement planning advice, it’s not just what you’ve saved, but how you utilise it, that can make all the difference to a successful retirement.

Now let’s consider a different scenario. Mrs Omelette is also age 67, and has just retired with full state pension, which supports part of her total expenditure requirement of £55,000 per year. She has substantial investments as a result of long-term investing as well as the recent death of her husband, who left everything to her.

She has the following accounts:

- A general investment account with £100,000

- An ISA account with £200,000

- Personal pensions that have not yet been accessed with £700,000

The total value of her liquid investments is £1,000,000 and all of these accounts are invested in a Moderate portfolio (also known as a Balanced portfolio similar to Mr Scramble). Mrs Omelette also has a main residence worth £800,000.

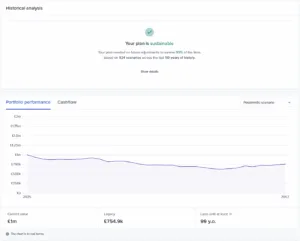

Based on a strategy of withdrawing income proportionately from each account, the cashflow forecast shows that in a pessimistic scenario, the plan will survive approximately 84% of the time, with a projection that at age 100 she will still have remaining investments of £268k.

So being able to afford her retirement is not so much of an issue for Mrs Omelette. The looming trouble for Mrs Omelette is that everything in her estate above £1m will be subject to Inheritance Tax (IHT) at 40% – which if her property value grows over the years (as one would expect it to), could include 40% IHT on all of her liquid investments. As we outlined in a recent article, from April 2027 the value of her estate will also include any pensions remaining on death.

For many clients with more substantial retirement savings, the significance of this change cannot be understated. Where once a pension was the last capital to be touched in retirement, because it could be passed on to others outside of the estate, now it may make sense to increase withdrawals from the pension, possibly even at 40% income tax rates, rather than suffer 40% inheritance tax on remaining funds, and then have your descendants still either pay their own marginal income tax rate on the remaining balance, or in turn also suffer 40% IHT on their death.

In the case of Mrs Omelette, this suggests a different use order of her capital, starting with taking income from pensions, and deferring withdrawal of her ISA until later. While this may incur greater income tax now, it is still more tax-effective than the total taxes suffered on death by the pension. The ISA can therefore be more aggressively invested because it is not intended to be used in the first 2 decades of her retirement (similarly to what was done for Mr Scramble, the later and earlier funds can be invested to balance out the overall risk of their portfolio). The upshot of this is likely to be two different successes in her retirement planning:

- first, an increased overall legacy but in a form which can be withdrawn entirely tax free in later years, and

- second, potentially a reduced IHT bill as the pension is utilised first and known taxes paid now rather than unknown but potentially greater amounts being paid later by beneficiaries.

Do YOU have clarity about your retirement withdrawals strategy?

What changes have you made to your financial plans lately? How have the changes to inheritance tax and pensions been factored into your retirement planning?

If you’d like to discuss achieving peace of mind around your retirement, please book a free initial chat here: https://calendly.com/duncan-bw-hoebridgewealth/30min

Download our free guide to retirement planning here: https://hoe-bridge-wealth.kit.com/guide-retirementplanning

NOTE: None of the above is financial or investment advice and you should speak to me or someone else professionally qualified to give you advice specifically tailored to your circumstances. Your capital is at risk. The value of your investment (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances. The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates and tax legislation may change in subsequent Finance Acts.

Book a free introduction chat

Book a free introduction chat