31 Dec 2025

Investment: Why is Liquidity the first building block of a solid financial plan?

Through the lens of the festive season and New Year, it’s tempting to consider liquidity as something to be measured in large glasses, or served in front of a warm crackling fire. However, in the world of finance, liquidity refers to how easily an investment can be turned into cash and banked or spent. This also has a lot to do with how easily something can be traded on an open market in order to turn it into cash.

Consider the list below – in what order would you rank them from most liquid to least liquid (least able to be converted quickly into cash)?

- Physical property – such as a buy-to-let property

- A one-month treasury gilt from the UK government

- Shares or units in a fund made up of global equities – shares of companies from around the world

- One-year fixed deposit cash interest account – no break permitted

- Physical gold – e.g. coins

- Shares in a large publicly traded company

- Minority share in a private business

- Shares or units in a property investment fund

- Bank current account

- A 5-year treasury bond from the US government

- Cash ISA (Individual Savings Account) with instant access savings

Here’s my suggestion on groupings:

Liquid = cash or near-cash: I, K

Slightly Illiquid = could take a few days to turn into cash: B, C, E, F, J

Less liquid = may take several months or even longer: A, D, G

Do you agree?

A word on Property Investment Funds (H) – these are liquid when all is well, but if a lot of investors want their money back at the same time, then they may be ‘gated’ or closed for trading while the fund sells assets such as physical buildings in order to return investor funds. In which case they can become very illiquid. (This for example was the downfall of the Woodford Fund, which hurt many investors when it collapsed after taking on too many illiquid investments).

As someone who once lived on the Gold Reef of South Africa, I will also note that gold has an interesting appeal for some investors – but it also has a mixed profile of who will actually buy or sell it in physical form, and therefore often has associated storage or security costs (and is subject to Capital Gains Tax on sale).

A typical feature of less liquid assets is that they are much more difficult to sell off in chunks – needing to be either completely sold off or not at all. Think for example of the difference between selling down a small portion of an equity or bond portfolio, which is done millions of times each day by individuals and also large pension funds, compared with trying to sell only a portion of a house. Another liquidity consideration is that an asset may have a very limited marketplace – for example most private company shares have a narrow range of people willing to take on the risk of buying them.

When we assess the riskiness of an investment, liquidity is one of the factors to be considered. An investment that is less liquid should generally be expected to offer higher average returns as a reward for this risk.

In personal finance, liquidity is closely linked with household cashflow and well-being. The Financial Conduct Authority (FCA) carried out a national Financial Lives survey which suggested that nearly 10% of the UK population have no cash savings at all, while another 21% had less than £1,000 of reserves to cope with any unexpected emergency. Responses to the survey suggested that nearly 12 million people feel stressed or overwhelmed dealing with financial matters (Footnote 1).

The personal finance hierarchy of needs that I suggest to clients (see below) prioritises ensuring that you have an adequate cash reserve to see you through a rough patch or a minor emergency, before you get too ambitious about other investments.

Liquidity is also something that adjusts at different ages and stages of life. When you retire, and don’t have working income and are instead living off your investments, then added liquidity in the form of increased cash reserves, may be an important buffer, financially and also psychologically, if markets go through a bad downturn for a while.

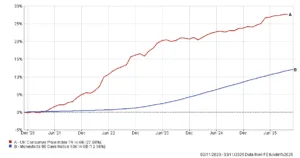

However, here in the UK in particular, many older people make the opposite mistake: becoming so averse to investment risk that they hold too much in cash. There is a false sense of comfort here because cash is readily at hand, but over time the spending power of that cash is eroded by inflation. See below a financial analysis of the change in value of Consumer Price Index (a common measure of inflation) compared with returns from 90-day cash deposits, over the last five years. This shows clearly how inflation outstrips cash held in a bank. So all things are best in moderation, including liquidity.

Having a clear strategy for your personal finances means ensuring that you tackle things in the best order possible: starting with liquidity, but also moving on to longer-term financial goals.

How do you prioritise your different financial goals?

If you want to discuss your investment strategy, or wider financial and retirement planning – book a free initial chat with me:

https://calendly.com/duncan-bw-hoebridgewealth/30min

NOTE: The value of your investment can go down as well as up. Past performance is not a reliable indicator of future results. None of the above is financial or investment advice and you should speak to me or someone else professionally qualified to give you advice specifically tailored to your circumstances.

Footnotes

Book a free introduction chat

Book a free introduction chat